Trading options presents both opportunities and significant risks for retail traders, who are individuals using personal funds to buy and sell market securities, typically trading part-time with smaller account sizes and limited access to professional tools (Reider, 2024). Unlike institutional investors, these retail traders lack formal training and are young, inexperienced, and low-income. Historically, accredited investors mainly traded options but with loosening permission level requirements and the rise of commission-free mobile platforms like Robinhood, options trading has become more speculative, drawing in retail traders who do not fully understand the risks involved. This shift, driven by aggressive marketing campaigns, social media-driven strategies, and easy access to leveraged products, has created a predatory market environment in which inexperienced traders face disproportionate risks.

While options offer tools for hedging and potential returns, their complexity often exposes uninformed participants to substantial financial losses. Many retail traders, lured by promises of quick profits, enter the market with unrealistic expectations viewing options trading as a shortcut to wealth only to experience repeated losses due to a lack of understanding. Unfortunately in the world of trading there is the “Rule of 90”, which suggests that 90% of traders lose 90% of their money within 90 days of trading (TrendSpider, 2025). Without proper training, retail traders are especially prone to impulsive and costly mistakes. The negative effects of options trading are exemplified by Alex Kearns, a 20-year-old Robinhood user, who took his own life after mistakenly believing he owed over $730,000 from a pending leg of an unsettled spread trade (Popper, 2020).

SmartOptions’s mission is to help retail traders become successful in options trading. SmartOptions is a Fintech platform designed to make options trading more accessible, transparent, and educational for retail traders. It addresses systemic challenges such as financial illiteracy, high risk trading practices, and market complexities by integrating real-time insights. Unlike traditional brokerage firms, it functions more like an advisory system, bridging the gap between education and execution to help retail traders make informed decisions. From the time retail traders sign up with a brokerage to the time they file their taxes, they are responding to a series of complicated questions which ultimately impact their performance. SmartOptions has been designed in mind to help retail traders make more strategic decisions through a dynamic, educational and data-driven approach.

Rise of Options Trading

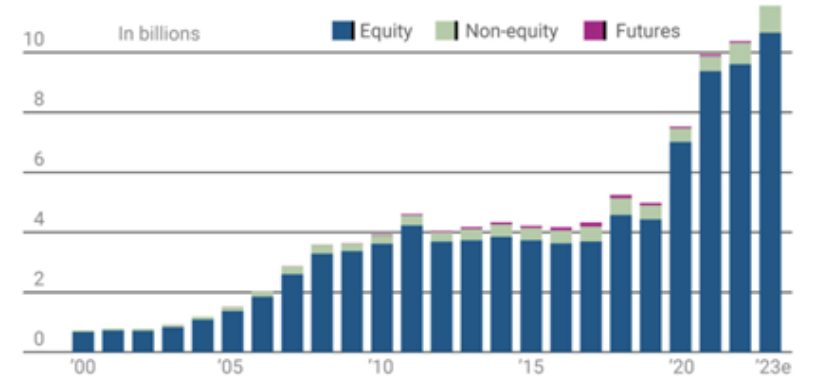

Global volume in options trading has exploded over the last decade, largely fueled by an increase in retail participation. This trend is particularly evident in emerging markets like India, where options trading has grown over 52% a year since 2013 with a staggering 85 billion contracts traded in 2023. The U.S. ranks second with 11% annual growth rate, from 4 billion contracts traded in 2013 to 11.2 contracts traded in 2023 (Futures Industry Association, 2023).

Figure 1: Total U.S. Options Volume

Note: From Investor’s Business Daily. (2023, April 26). Options trading today after 50 years of growth.

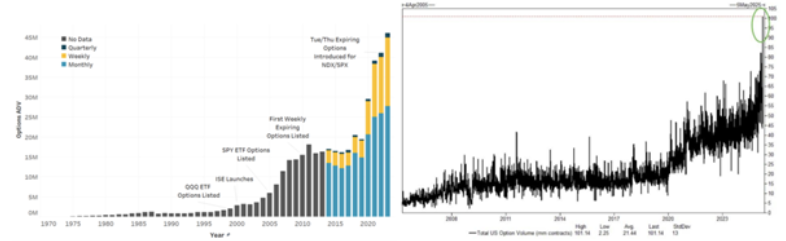

The average daily volume (“ADV”) of option contracts has risen sharply from approximately 16 million in 2013 to 45 million in 2023 (Figure 2) concentrated in a small number of very liquid Single Stocks (52%), ETFs (39%), and Indices (9%). Options expiring within a week make up 35% of ADV, while monthly expiries account for 62%, and quarterly options represent the remaining 3% (Mackintosh, 2023). The notional value of this ADV has also surged, climbing from $875 billion per day in 2020 to $2.1 trillion in 2023. Open interest has followed a similar trend, with the average notional value of open positions rising to $616 billion per day in 2024, up from $480 billion in 2023 and $280 billion in 2020 (Acworth, 2024). As shown in Figure 3, total options ADV has spiked to an unprecedented 100 million contracts traded in 2025, with no signs of slowing down.

Figure 2: Options ADV by Expiration Figure 3: Options Volume

Note. From “What’s Driving the Growth in Options Trading,” by P. Mackintosh, 2023, Nasdaq. | Note: From SpotGamma. (2025, April 7). options volume friday [Tweet]. X.

Rise of the Retail Trader

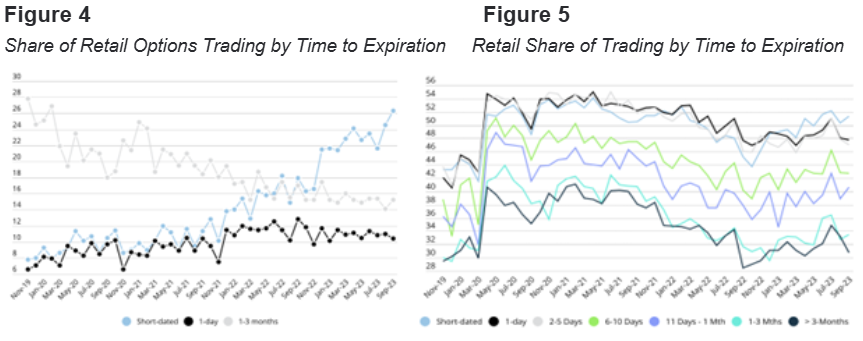

Retail investors have significantly increased their presence in the options market. Their share of total options volume grew from 35% at the start of the COVID-19 pandemic in March 2020 to nearly 45% by the end of 2023, a remarkable shift in a market historically dominated by sophisticated investors. The rise of retail options traded coincided with growing popularity of short-dated options, reflecting retail traders’ preference for contracts with brief expiration periods. From November 2019 to September 2023, short-date options increased from 8% to 26% of all retail trades (Figure 4) while retail options with five or less days to expiration increased from 35% to over 56%. Figure 5 shows that by September 2023, retail made up 52% of short-dated trades versus 31% of trades greater than 3 months (Poser, 2023).

Note. Adapted from “What’s Driving the Growth in Options Trading,” by P. Mackintosh, 2023, Nasdaq.

SmartOptions is designed for retail traders, individual investors who use personal funds to trade securities for supplementary income. Unlike professional or institutional investors, such as hedge funds and proprietary trading firms, retail traders typically operate with smaller capital bases, trade part-time from home, and lack advanced analytical tools. These traders are predominantly young and tech-savvy but inexperienced. In fact, a 2021 FINRA survey reported 38% of new brokerage accounts were from first-time investors with 22% between ages 18 and 29, 66% under 45 years old, and 33% holding account balances of less than $500 (Bryzgalova, 2023). Trading applications like Robinhood reported a median user age of approximately 31 years (Moise & Singh, 2021) and a median account balance near $4000 (BusinessofApps, 2025). Moreover, Apex Clearing data reveal that 17% of Apex Clearing’s new accounts in 2020 were opened by customers with an average age of 19 (Apex, 2018). These demographic characteristics, combined with SEC observations of impulsive decision-making, underscore the need for a platform that integrates trading execution and tailored education (Craig, 2021).

Predatory Market Environment

Dumb Money

The broker-dealers and market-makers profit from what industry insiders often call “dumb money”: high volume Payment For Order Flow (“PFOF”) transaction fees, excessive use of leverage, high-risk strategies, and inflated spreads and that eventually leave retail traders with depleted capital unable to continue trading (International Journal of Research in Commerce, 2023).

High volume PFOF: The gambling-like appeal of options trading creates perfect conditions for volume-focused business models. The emphasis on volume over trader success has fostered a market ecosystem that can be characterized as predatory. Like lottery systems that maximize revenue through frequent ticket sales, broker-dealers employ multiple strategies to attract and retain customers (Bryzgalova, 2023). These include zero-fee commissions, aggressive marketing campaigns, ease of mobile trading, fractional trading, social features, referral programs, celebrity promotions, and gamified design elements such as confetti celebrations (Securities and Exchange Commission, 2021). Robinhood, for example, lists more risky short-term weekly options as the default on their trading app (Bryzgalova, 2023). Robinhood’s strategic implementation of these tactics accelerated industry adoption; during the first quarter of 2020, Robinhood earned $18,955 on 25,840 options contracts traded for every dollar in their average customer account, far surpassing $1881 earned on 2,188 contracts for TD Ameritrade (Popper, 2020).

Excessive Leverage: The options trading ecosystem effectively capitalizes on inexperience, drawing retail traders in with the promise of leverage. While leverage allows small investments to control large positions, it also magnifies losses, rapidly depleting capital (Barber & Odean, 2000). Although regulations require broker-dealers to assess new customers’ experience, financial situation, and risk tolerance, many conduct only cursory reviews to accelerate customer acquisition while offering accounts with margin trading capabilities (Financial Industry Regulatory Authority, 2022). These new customers are often unprepared for their permission levels and the magnified losses that can come with leverage.

High-Risk Strategies: Accompanying retail order flow is retail trader’s strong preference for inexpensive, weekly options that tend to lose money on average. In aggregate, assuming a ten day holding period, retail traders lost $2.1 billion from November 2019 to June 2021. These losses were concentrated in buy trades, at-the-money contracts (72% of trades), call contracts (69% of trades) and options with less than a week expiry (Bryzgalova, 2023).

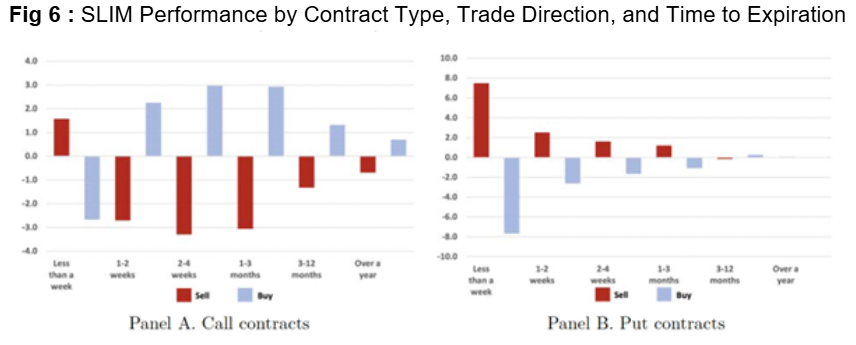

Pavlova and Bryzgalova, in Retail Trading in Options and the Rise of the Big Three Wholesalers (2023, Journal of Finance), introduce the SLIM methodology to identify retail trading in options by isolating wholesaler-intermediated single-leg trades executed through price improvement auctions, using newly introduced OPRA transaction flags. Figure 6 plots the 10-day net performance of SLIM buy and sell trades, showing that for options expiring in less than a week, buyers of both Put and Call contracts incur significant losses, while sellers of puts and calls realize substantial gains.

Note. Adapted from Retail Trading in Options and the Rise of the Big Three Wholesalers, by S. Bryzgalova, A. Pavlova, and T. Sikorskaya, 2023, Journal of Finance (forthcoming)

Behavioral Challenges

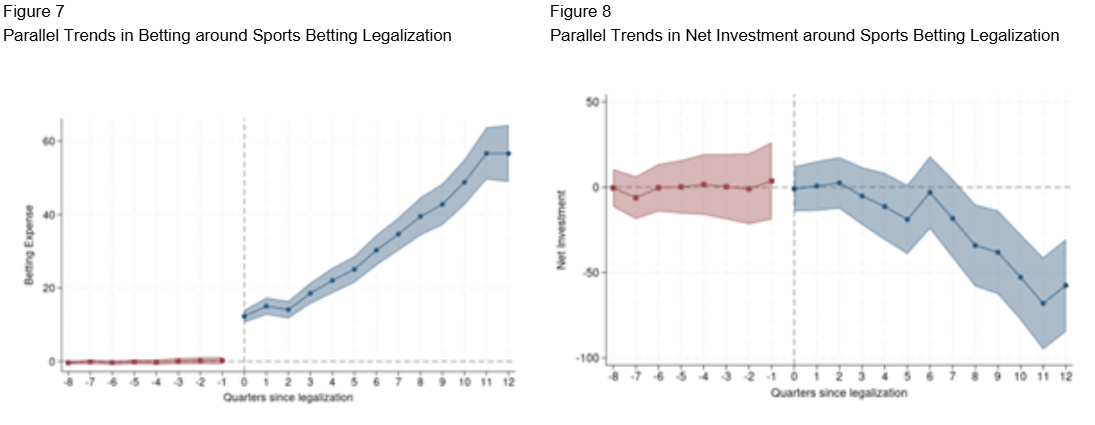

The explosive growth in options trading has introduced concerning parallels to gambling behavior, especially for new retail traders. Options trading has followed a wave of gambling mania since the US Supreme Court overturned a Federal ban on sports betting in 2018. Like sports betting, retail traders are drawn into the excitement and potential for high risk, high rewards at the opportunity costs of making more prudent investment choices (Baker et al., 2024). Figures 7 & 8 depict this distinctive trend showing average households betting expenditures increasing $4.60 per quarter while net investments decreasing $9.00 per quarter following the legalization of sports betting.

Note: These figures present event-time coefficients of the effect of the legalization of sports betting on sports bets (e.g., deposits to sports betting apps) on net investment (e.g., deposits less withdrawals at equity brokerages).The x-axis shows quarters around sports betting legalization (𝑡 = 0 at online launch), the y-axis shows the average causal effect on deposits and net investment, and the shaded region indicates the 95% confidence interval. Adapted from Smith, J., & Johnson, A. (2023). Gambling Away Stabilitya: Sports Betting Impact on Vulnerable Households.

While betting increases sports-related consumption and entertainment value, it crowds out positive financial behaviors like investing and saving, increasing borrowing, credit card debt and overdrafts for economically vulnerable households with below median savings and high overdrafts (Baker et al., 2024). As Baker et al. (2024) note: “Marketed as a form of entertainment, the industry’s profitability suggests that the typical bettor faces negative expected returns. Moreover, evidence from other gambling contexts indicates that bookmakers exploit bettors’ cognitive biases and lack of skill, making betting a detrimental financial activity for most households.”

Using transaction-level data from over 230,000 U.S. households and a staggered fixed effects difference-in-differences framework, Baker finds low-savings households have 32% higher sports betting spend-to-income ratio than high-savings households. In addition, despite lacking financial stability, the study shows $1 spend on sports betting for economically constrained households leads to a $3 decrease in investments and savings (Baker, 2024). It categorizes trading options, along with crypto, as gambling behavior similar to sports betting, and suggests that excitement in betting leads to more engagement in speculative financial market activity like options trading.

Unlike traditional buy-and-hold strategies, options trading involves greater leverage, heightened price sensitivity, and shorter time horizons (Australian Securities and Investments Commission, 2020). Retail traders often fail to account for time decay, implied volatility, and other factors inherent in complex derivatives (Finance Strategists, n.d.). The complexity involved in options trading can lead to behavior that resembles gambling, with traders doubling down on losses and pursuing speculative strategies with little regard for risk management (Baker et al., 2024). The U.S. Securities Exchange and Commission (SEC) protects retail investors, including options traders, through disclosure requirements, oversight of broker-dealers via FINRA, and enforcement of fair dealing and suitability standards. While disclosure remains the core strategy, its effectiveness is limited, and the SEC’s enforcement efforts often struggle to keep pace with evolving risks.

Behavioral finance has shed light on the cognitive and emotional biases that amplify these risks (Mercer Advisors, n.d.). Kahneman and Tversky’s Nobel Prize-winning Prospect Theory (1979) states that individuals overvalue losses relative to gains, leading to irrational risk-taking after experiencing a drawdown. Salience Theory shows people are drawn to positive skewed outcomes that have low probability but outstanding payoffs (Bordalo, 2012). Further studies reveal the disposition effect, where traders prematurely sell winning positions and hold onto losers in the hope of recouping losses (Shefrin & Statman, 1985). Overconfidence, a bias linked to excessive trading, has been found especially prevalent among retail traders, who may overestimate their skill or knowledge of market conditions (Barber & Odean, 2000; IJRC, 2023). Retail traders who lack structured guidance or accountability mechanisms are more likely to engage in emotionally driven trades, jeopardizing long-term returns (IJPR, 2023). Research increasingly points to the importance of ongoing personalized coaching, financial education, and real-time performance tracking as effective mitigants against irrational trading behavior (IJRC, 2023). The market is overdue for a comprehensive solution like SmartOptions that addresses the behavioral aspects of this problem.

Market Structure

Payment For Order Flow

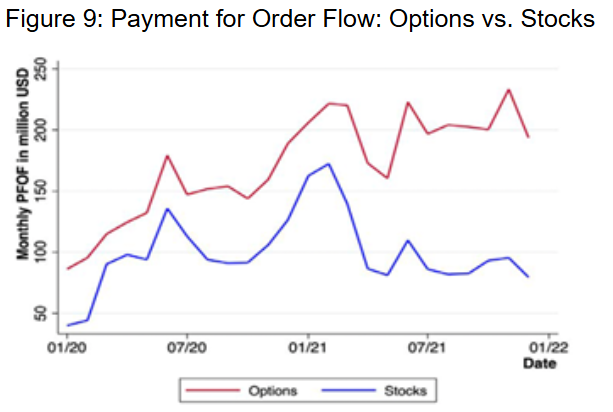

Retail brokerages typically route client orders to financial intermediaries known as wholesalers, who coordinate with market makers to fulfill the trades. These arrangements aren’t based strictly on getting the best price for each trade, but rather on the overall economic agreement with the broker receiving payment for order flow (“PFOF”) and the client often receiving some level of price improvement (Bryzgalova, 2023). The sheer volume of options feeds (over 1 million) compared to stocks (approximately 10,000) means an exchange is less likely to have limit orders on its order books, making market makers the primary source of liquidity (Financial Markets Authority, 2022). Thus, the majority of PFOF for U.S. brokerages comes from options, not equities, with 2021 seeing $2.4 billion PFOF for options and $1.3 billion PFOF for equities. Figure 9 illustrates the monthly difference, with PFOF reaching $200 million for options and approximately $75 million for stocks by December 2021, a striking gap of $125 million.

Note: Adapted from: Bryzgalova, S., Pavlova, A., & Sikorskaya, T. (2023, September 3). Retail trading in options and the rise of the big three wholesalers. Journal of Finance (forthcoming)

Note: Adapted from: Bryzgalova, S., Pavlova, A., & Sikorskaya, T. (2023, September 3). Retail trading in options and the rise of the big three wholesalers. Journal of Finance (forthcoming)

Payment for order flow (“PFOF”), a practice made infamous by Bernie Madoff, creates hidden costs for retail traders, leading to poor execution quality and institutional advantages. These advantages were most famously exemplified by the GameStop trading halt in 2021 where retail traders, due to volatility and settlement risk, faced trading restrictions that ultimately benefited institutional investors (U.S. Senate Banking Committee, 2021). PFOF distorts incentives, reduces transparency, and often costs more than it saves. Despite offering commission-free trading, brokers like Robinhood delivered such poor trade execution from 2016 to 2019 that clients would have been better off paying commissions elsewhere. Regulators around the world are catching on as the UK and Canada have banned it while the EU will follow in 2026 and the U.S. is planning reforms (Nasil, 2024).

Equity Markets: In equity markets, wholesalers often match orders on proprietary trading systems rather than public exchanges, effectively shielding them from competition by other market makers. To meet best execution requirements, retail brokers often route orders to wholesalers who provide slight price improvements over the National Best Bid and Offer (NBBO). Since the NBBO is standardized across brokerages, this allows trades to avoid public exchanges and remain largely undisclosed. This is known as internalization which has been criticized for reducing liquidity, price discovery, and widening bid-ask spreads.

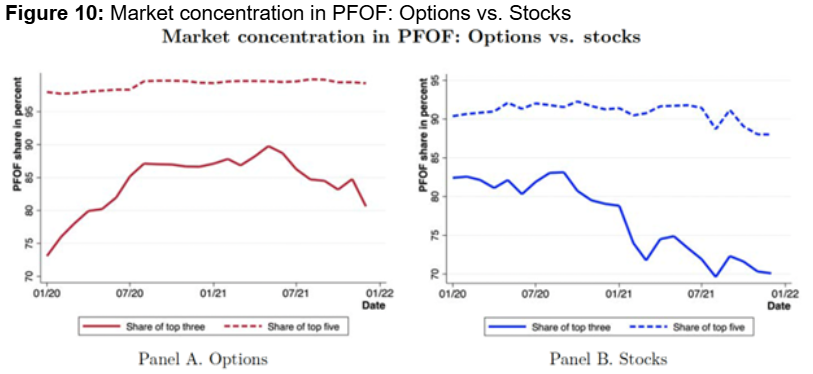

Options Markets: In option markets, wholesalers are required to route orders exclusively to public market exchanges for execution, which in theory prevents internalization and promotes open market competition. In reality, however, the majority of retail options order flow is internalized indirectly with minimal market competition. As Figure 10 illustrates, competition is further deteriorated by the large concentration of order flow to only a few wholesalers, with 95% coming from the top five and approximately 85% coming from the top three (Citadel, Susquehanna, and Wolverine).

Note: The top three wholesalers in options are Citadel, Susquehanna, and Wolverine, while the top three wholesalers in stocks are Citadel, Virtu, and Susquehanna. Adapted from: Bryzgalova, S., Pavlova, A., & Sikorskaya, T. (2023, September 3). Retail trading in options and the rise of the big three wholesalers. Journal of Finance

Note: The top three wholesalers in options are Citadel, Susquehanna, and Wolverine, while the top three wholesalers in stocks are Citadel, Virtu, and Susquehanna. Adapted from: Bryzgalova, S., Pavlova, A., & Sikorskaya, T. (2023, September 3). Retail trading in options and the rise of the big three wholesalers. Journal of Finance

Non-Competitive Execution

Most options trades fail to achieve the best possible pricing because they are not executed in fully competitive markets. The majority of retail options orders are routed through systems structured to favor brokers and wholesalers rather than individual traders. Across the options market, the different execution methods described in detail below offer varying degrees of competition, transparency, and price improvement, often leaving retail traders at a disadvantage.

Public Exchange Order Books (~35%): High Competition

- The default execution method where retail orders are routed to public exchange order books, which are fully transparent and matched against the best available prices (NBBO), although brokers may still collect small fees or rebates for these trades (U.S. SEC, 2020).

Direct / Internalized Orders (~30%): Low Competition

- Facilitation / Internal Crossing (10%): Common for institutional and block trades, this execution method involves brokers routing retail orders to specific wholesalers and their affiliated market makers, often through facilitation or internal crossing mechanisms where the counterparty is prearranged, limiting public competition (Cboe Global Markets, n.d.).

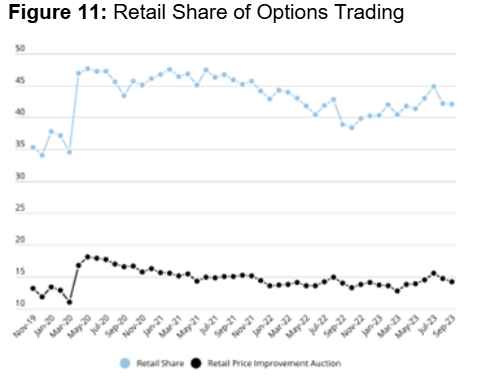

- Price Improvement Auctions (15%): Price Improvement Auctions (PIAs) allow wholesalers to internalize retail orders through price auctions that must meet or beat the NBBO. In practice, wholesalers coordinate with affiliated market makers to present paired orders to a PIA on an exchange, giving third parties only a brief window to submit better bids. High exchange fees, designed to protect these relationships, discourage outside competition. As a result, wholesalers and their affiliates usually win, keeping execution semi-private, limiting true price improvement, and leaving public spreads wide (U.S. SEC, 2022). Figure 11 shows that retail traders account for 45% of total options volume, with Price Improvement Auctions (PIAs) representing 15% of total volume and one-third of all option retail trading activity (Mackintosh, (2023).

Note. Adapted from “What’s Driving the Growth in Options Trading,” by P. Mackintosh, 2023, Nasdaq.

Complex Order Books (~30%): Moderate Competition

- Complex Order Books (COBs) route most multi-leg options strategies (e.g., spreads) to specialized exchange engines without a price improvement auction. While orders are exposed to some market participants, the absence of mandatory public bidding limits competition compared to fully open single-leg markets (Cboe Global Markets, n.d.).

Floor Trading (~5%): Low competition

- Floor Trading represents a very small share of options volume and relies on an antiquated open outcry method, mostly used on select exchange floors for institutional block trades. Competition is low because trades are negotiated manually between a limited number of participants, without broad public exposure or electronic price discovery (Cboe Global Markets, n.d.).

While some orders reach highly competitive public exchanges, a significant share of retail options flow is routed through semi-private or internalized mechanisms, limiting true price competition and weakening execution quality. To address this challenge, SmartOptions offers a core feature specifically designed to combat poor execution and high spreads, detailed further in a subsequent section (“Pillar 2: Execution”).

→ Continue Reading to Part 2: SmartOptions’ Three Pillars