In 2017, SoftBank invested $250M in Kabbage at a $1.2 billion valuation. Three years later, American Express acquired what remained for $850M — excluding the loan portfolio entirely.

What happened?

This isn’t just a story about a pandemic crushing a lender. It’s about the gap between headline valuations and the math that should drive them. When I was building financial data platforms, I saw this pattern repeatedly: exciting growth stories valued on narrative rather than downside-adjusted fundamentals.

Let’s break down how a disciplined VC should have valued Kabbage using the VC Method — and what that reveals about late-stage venture risk.

What Made Kabbage Interesting

Founded in 2009, Kabbage wasn’t a traditional lender. Instead of credit scores and tax returns, it used real-time signals: QuickBooks data, e-commerce transactions, social media activity, even macro indicators.

The thesis was compelling:

- Every industry has its own financial rhythm

- Restaurants don’t behave like construction companies

- Seasonal businesses don’t behave like subscription businesses

- Better data = better underwriting = lower defaults

It was a powerful idea in an underserved market. The question was: what was it actually worth?

How VCs Actually Value Companies: The VC Method

Most valuation frameworks start with today’s performance. The VC Method works backward from the exit.

Why? Because VCs don’t make money on revenue growth — they make money on exits. Their question isn’t “What’s this worth today?” but:

“If this succeeds, what could it exit for — and what return does that give me?”

Here’s the framework:

Step 1: Estimate Terminal Value

What will the company be worth at exit?

For Kabbage, a good comparable was OnDeck, which IPO’d in 2014 at $1.32B. Given Kabbage’s superior data infrastructure, assume a $2B exit in 5 years.

Terminal Value (TV) = $2,000M

Time to exit (t) = 5 years

Required return (r) = 30%Why 30%? VCs use high IRRs (25–50%) not out of greed, but because:

- Most startups fail

- Returns must cover portfolio losses

- Capital is illiquid for years

- Fund timelines are finite

Step 2: Discount to Present Value

Apply the required return to bring that future value back to today:

Discounted Terminal Value (DTV) = TV / (1 + r)^t

DTV = 2,000 / (1.3)^5

DTV = $538.7MThis is the “risk-adjusted future value” — it assumes both upside potential and the reality that the path is dangerous.

Step 3: Calculate Required Ownership

If a VC invests $250M:

Required stake = Investment / DTV

Required stake = 250 / 538.7 = 46.4%Translation: To justify a $250M check, the VC must own ~46% of Kabbage at exit.

This is why late-stage rounds are so dilutive — the math demands it.

Step 4: Calculate Valuation

Post-money valuation = Investment / Required stake

Post-money = 250 / 0.464 = $539M

Pre-money = Post-money - Investment

Pre-money = 539 - 250 = $289MSo the disciplined valuation for Kabbage’s Series F would be $289M pre-money, not $1.2B.

The Critical Part Founders Miss: Future Dilution

No VC assumes their round is the last. This is where most founders (and some VCs) get the math wrong.

If Kabbage planned a $100M Series G the following year, that investor would need ~10.4% ownership (using a 20% IRR over 4 years to the same $2B exit).

That future round dilutes the Series F investor. So the Series F investor must start with more ownership to end where they need to be:

Retention ratio = 1 / (1 + future dilution)

Retention ratio = 1 / (1 + 0.104) = 0.906

Adjusted ownership needed = 0.464 / 0.906 = 51.2%This changes everything:

Post-money = 250 / 0.512 = $488M

Pre-money = 488 - 250 = $238MFuture rounds force today’s valuation down. The fully diluted, forward-corrected valuation is $238M — not $1.2B.

How This Maps to Actual Shares

Venture math isn’t complete until it translates to cap table mechanics.

Assuming 5M existing shares before Series F:

New shares issued (Series F) = (0.512 × 5M) / (1 - 0.512) = 5.25M shares

Price per share (Series F) = $250M / 5.25M = $47.66

Total shares after F = 10.25MFor Series G:

New shares issued (Series G) = (0.104 × 10.25M) / (1 - 0.104) = 1.19M shares

Price per share (Series G) = $100M / 1.19M = $84.36

Total shares after G = 11.43MSeries G is an up round ($84.36 vs $47.66), even though it’s dilutive. This is normal in healthy growth companies.

What Actually Happened

SoftBank invested $250M in 2017 at a $1.2B valuation — more than 5x what the VC Method suggested.

By 2020:

- COVID devastated small businesses

- Loan defaults spiked

- Lending operations took massive losses

- Kabbage laid off staff and stopped lending

- The loan book became too risky to acquire

American Express bought the company for ~$850M, excluding the loan portfolio.

For SoftBank, this was a down-round exit — their stake was worth less than their entry valuation.

Why This Matters Beyond Kabbage

The VC Method forces clarity on five critical questions:

- What must the company be worth at exit?

- How likely is that outcome?

- How much ownership is required?

- How will future rounds dilute that stake?

- Does the check size make sense?

It’s not a prediction. It’s a belief system translated into math.

In Kabbage’s case, even well-structured math couldn’t anticipate a pandemic. But the valuation gap suggests the investment thesis was built on best-case assumptions rather than risk-adjusted returns.

Having built a financial data platform myself, I learned that the hardest part isn’t modeling the upside — it’s being honest about what has to go right for the upside to materialize. Kabbage’s model required perfect credit performance in an inherently risky segment. When the macro environment shifted, there was no margin for error.

What Founders Should Negotiate Beyond Valuation

Headline valuation is seductive, but here’s what matters more:

- Liquidation preferences: 1x is standard, 2x+ means investors get paid first in down scenarios

- Anti-dilution protection: Weighted average is fair; full ratchet is punitive

- Board composition: Control matters more than ownership percentage

- Investor quality: Who helps during hard times vs. who demands their money back first

A $300M valuation with clean terms often beats a $1B valuation with structured preferences.

The Valuation Formula Reference

| Concept | Formula | Kabbage Example |

|---|---|---|

| Terminal Value | Projected exit value | $2,000M |

| Discounted Terminal Value | TV / (1 + r)^t | $538.7M |

| Required Final Stake | Investment / DTV | 46.4% |

| Post-Money Valuation | Investment / Ownership | $538.8M |

| Pre-Money Valuation | Post-Money – Investment | $288.8M |

| Retention Ratio | 1 / (1 + Future_Ownership) | 0.906 |

| Adjusted Ownership | Required_Final / Retention | 51.2% |

| New Shares Issued | (Ownership × Existing) / (1 – Ownership) | 5,245,902 |

| Price Per Share | Investment / New_Shares | $47.66 |

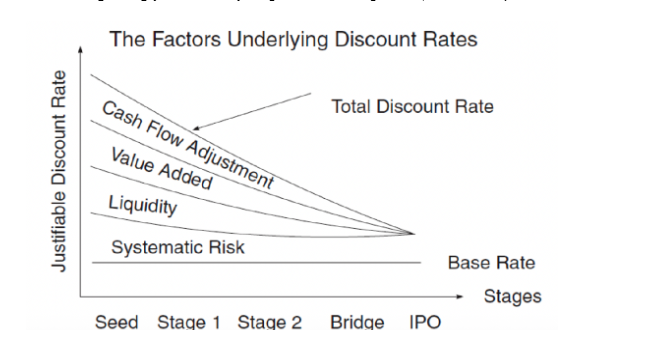

Typical VC Discount Rates by Stage

| Stage | Target IRR | Why |

|---|---|---|

| Seed | 60%+ | Highest risk, least proven |

| Series A | 40–60% | Product-market fit unclear |

| Growth | 30–50% | Proven model, scaling risk |

| Late Stage | 20–35% | Lower risk, approaching exit |

Visualizing Why Discount Rates Decline

As companies progress through stages, multiple risk factors decline: liquidity improves, systematic risk decreases, and less value-add is needed from investors. The combined effect is a lower required IRR.

The Bottom Line

Valuation isn’t about today. It’s about what must be true in the future for an investment to make sense.

SoftBank’s $1.2B valuation required Kabbage to exit at $4-5B+ to generate venture-scale returns. The VC Method math suggested $238-289M was more defensible.

The gap between those numbers? That’s where risk lives.

And in venture capital, risk always finds a way to show up.